What to Do with an Inheritance: Smart Steps to Secure It

Did you know? Over 70% of wealth transferred through inheritance is lost within the second generation, according to recent studies. This startling statistic underscores why knowing what to do with an inheritance is crucial for your financial security and your family's legacy. Whether your inheritance is modest or sizable, the most important steps to protect this windfall happen in the first 90 days—decisions now will determine if your inheritance grows or disappears. This guide brings you an informed, action-oriented plan to help you safeguard and maximize your inherited assets, avoid costly mistakes, and set yourself up for lasting success.

A Surprising Statistic: The Need for Informed Inheritance Decisions

It’s easy to underestimate the complexity of receiving an inheritance. Research indicates that 70% of people lose their inherited wealth within a single generation. The reality is, without a structured approach to what to do with an inheritance, financial missteps such as impulse spending, missed tax deadlines, and poor planning can quickly erode decades of family savings. When you receive an inheritance, you’re not just getting money—you’re stepping into a web of legal, tax, and financial decisions that require careful navigation.

Inheriting assets—be it cash, real estate, stocks, or retirement accounts—comes with a host of obligations. You may need to pay taxes such as estate tax, inheritance tax, or face capital gains tax if you sell inherited property or securities. If you don’t take time to understand these factors, you risk costly errors that could drastically shrink your inheritance. That’s why having a concrete plan—built on expert advice and sound strategies—should be your first step after you receive an inheritance.

Why Many Lose Their Inheritance (and How to Avoid It)

It’s a sobering reality: the vast majority of inherited wealth fades because beneficiaries rush into decisions, underestimate tax liabilities, or lack a clear financial plan. When you suddenly gain a sum of money—large or small—temptations and emotions can cloud your judgment. It’s common for people to splurge on luxury purchases, help friends and family without a clear boundary, or invest in unfamiliar markets. Many also forget to budget for the estate tax, inheritance tax, and capital gains tax that can arise from selling inherited assets, especially real estate or mutual funds.

To ensure you don’t fall victim to these pitfalls, it’s important to pause, assemble your financial and legal documents, and seek professional guidance. Knowing the tax rules about your specific situation—such as how cost basis affects capital gains if you sell stocks or a home—is crucial. This guide offers you a step-by-step roadmap to avoid those mistakes, protect your financial future, and honor your family’s legacy.

What You'll Learn in This Guide to What to Do with an Inheritance

- A step-by-step 90-day action plan for effectively managing an inheritance

- Key concepts such as estate tax, inheritance tax, and capital gains tax

- How to safeguard your inheritance by choosing between savings, investments, and paying off debt

- Mistakes to avoid after you receive an inheritance

- When it’s wise to consult a financial advisor about your inheritance

Step 1: Pause and Assess Before Deciding What to Do with an Inheritance

Receiving an inheritance can be overwhelming. It’s tempting to spring into action, but the most critical first step is to pause and assess. Allowing emotions to settle helps you avoid the most common mistakes, such as rushed spending or investment, before you fully understand the implications. During this phase, gather all related documents—such as wills, account statements, deeds, and recent tax returns. This documentation is essential for identifying your full suite of inherited assets and potential tax liabilities, including possible estate or inheritance tax owed at the local, state, or federal level.

Equally important is educating yourself about your financial and tax obligations. Inheritances may come with complex reporting requirements and deadlines, especially if you inherit assets like real estate, mutual funds, stocks, or an inherited IRA. Understanding whether you need to pay tax, and how to calculate your cost basis, can save you from unexpected surprises. Before making any financial decisions, slow down and consult with a tax professional or financial advisor who can help clarify your responsibilities and opportunities as an heir.

Let Emotions Settle: Avoid Hasty Financial Mistakes

Grief and excitement often go hand-in-hand after you receive an inheritance, making it easy to act impulsively. Financial decisions made in an emotional state are less likely to be in your long-term best interest. Take at least a few weeks to process the news before you do anything big with your inheritance. Don’t pay off debts, buy a new car, or invest in real estate right away. Instead, use this period to review the estate plan, read through the will, and seek support from trusted loved ones.

During this stage, jot down questions about your future—like whether you should prioritize your emergency fund or contribute to your retirement accounts. This initial pause allows you to avoid rushed purchases, avoid triggering unforeseen capital gains taxes, and gives you time to create a thoughtful, potentially life-changing, financial plan. Emotional clarity leads to stronger, more secure decision-making down the road.

Assemble Important Documents Related to the Inheritance

Your next practical step is to gather all documents connected to the inheritance. This includes the decedent’s last will and testament, trust documents, death certificates, current account statements, and titles or deeds to real estate or vehicles. If mutual funds, brokerage accounts, or retirement accounts are involved, collect the most recent statements for each. You’ll need these papers to claim your inheritance, understand its nature, and consult with a tax professional to clarify any pay tax or reporting requirements.

Having everything in one place streamlines your process for meeting deadlines, such as any tax reporting or estate settlement obligations. Carefully organized documentation will also help minimize delays and questions as you start making key financial decisions, such as whether to keep, sell, or invest inherited assets.

Gather Information About Estate Tax and Inheritance Tax Obligations

Before you do anything with your inheritance, research specific estate tax and inheritance tax rules that may apply to you. Some states charge an inheritance tax, in addition to possible federal estate tax. If you receive an inheritance from real estate, mutual funds, or stocks, you may later incur a capital gains tax if you sell those assets above your cost basis. Understanding these concepts now prepares you to avoid unexpected, hefty tax bills and ensures your decision-making is based on accurate net values rather than just the gross amount inherited.

Consulting a tax professional or financial advisor is crucial here. These experts can analyze your cost basis, project any capital gains or gains tax due if you decide to liquidate inherited assets, or clarify if inherited IRAs or retirement accounts have different tax treatment. With all your documentation and information in hand, you’re ready to move to the next key steps.

Step 2: Build Immediate Financial Stability with Your Inheritance

Once you’ve collected your inheritance paperwork and gained a basic understanding of your tax obligations, it’s time to use these new resources to create a foundation of financial security. Begin by shoring up your emergency fund—this means saving three to six months’ worth of living expenses in a highly liquid, low-risk account. A healthy emergency fund protects you from unexpected costs, such as job loss or medical bills, and gives you space to thoughtfully plan the next steps for your inheritance. For many, this is a rare opportunity to finally create a financial buffer after years of living paycheck to paycheck.

Next, prioritize paying off high-interest debts, like credit cards or personal loans. The interest rate on these obligations often dwarfs what you might earn from investments. Reducing your debt load immediately improves your financial flexibility and long-term security. Before making larger investment moves, assess your most pressing financial needs and ensure your basic financial safety net is in place. This sets you up for smarter decisions with the rest of your inheritance.

Create or Strengthen Your Emergency Fund with Your Inheritance

An emergency fund is your first line of defense against unexpected expenses. Use a portion of your inheritance to either establish or strengthen your savings account, targeting at least three to six months of your regular expenses. This is especially important if your prior financial plan didn’t include a robust emergency fund. An adequately funded emergency stash reduces stress, empowers you to make more thoughtful decisions, and minimizes the risk of needing high-interest credit card debt in a future emergency.

Consider opening a high-yield savings account—separate from your daily spending account—to grow your funds faster while retaining easy access. Avoid putting emergency savings in stocks, mutual funds, or other fluctuating assets, as their value might drop when you need cash most. Building your emergency fund is a concrete, immediate way to use your inheritance for financial peace of mind.

Pay Off High-Interest Debt with Inherited Funds

If you have outstanding debts with high interest rates—especially credit cards—using your inheritance to pay them off is usually a smart move. The interest rate on these cards often exceeds what you’d earn from conservative investments, and paying down debt brings instant, risk-free returns. Make a list of your debts by interest rate and balance, and prioritize those with the highest rates for repayment first. Reducing or eliminating these financial burdens gives you more free cash flow and greater peace of mind as you develop your long-term financial plan.

However, carefully weigh the trade-off between paying off debt and investing. Some debts, such as a low-interest-rate mortgage, may not be worth paying off early if you can earn a higher return elsewhere. Every financial situation is unique, so consult with a financial advisor before making significant changes. They can help you weigh gains taxes and other tax implications tied to your debt repayment strategy—especially if funds come from inherited IRAs or mutual funds with special tax rules.

What to Do with an Inheritance: Prioritize Your Short-Term Financial Security

After ensuring your emergency fund is intact and high-interest debts are paid down, evaluate any other urgent needs for your inheritance. For example, you might set aside a portion of inherited money to cover immediate family expenses, upcoming education costs, or medical emergencies. Focusing on short-term stability helps you avoid the pressure to make quick, risky investments or major purchases. The remaining portion of your inheritance can then be allocated toward your medium- and long-term goals with greater confidence and flexibility.

This phase is about creating financial stability, not maximizing investment return just yet. Your inheritance is a powerful tool for securing your present; by addressing urgent needs first, you’ll have a solid foundation for the strategic decisions ahead—whether that’s investing in real estate, mutual funds, or growing your retirement accounts.

Step 3: Evaluate Tax Implications When You Receive an Inheritance

One of the biggest misunderstandings around inheritances is how and when to pay taxes. Understanding the differences between estate tax, inheritance tax, and capital gains tax is essential for anyone who receives an inheritance, especially when dealing with complex assets like real estate, mutual funds, or inherited IRAs. Start by confirming which taxes apply based on your state, asset type, and the value of the inheritance. For example, only a handful of states levy an inheritance tax, while federal estate tax only kicks in above multi-million-dollar thresholds, but capital gains tax almost always applies when you sell inherited assets for more than their cost basis.

It’s also important to note that inherited retirement accounts—such as an inherited IRA or 401(k)—carry their own tax rules and required minimum distributions (RMDs). A tax professional or experienced financial advisor can help you calculate your cost basis and avoid hefty penalties. Whenever possible, consult with them as soon as you receive an inheritance to ensure you maximize the value and remain fully compliant with reporting requirements.

Understanding Estate Tax and Inheritance Tax Laws

For most Americans, federal estate tax is only a risk if the value of the estate is above $12. 92 million (in 2023). Estate tax is based on the total value of assets left behind by the original owner, with the tax being paid by the estate before assets are distributed to heirs. Inheritance tax, by contrast, is levied by some states based on the amount an individual receives from a deceased person's estate—so you might need to pay tax to your state before claiming your portion.

Understanding these nuances ensures you aren’t blindsided by a tax bill months after you receive your inheritance. Also, make sure to confirm if your inheritance involves jointly held property, real estate, or retirement accounts with unique state or federal tax treatment. For assets with uncertain value, such as real estate, obtain a professional appraisal to establish a fair market value—and, in turn, an accurate cost basis for potential gains tax calculations.

Capital Gains Tax, Gains Tax, and Their Impact on Your Inheritance

When you sell inherited assets, such as stocks, real estate, or mutual funds, you may owe capital gains tax if the sale price is higher than the asset’s cost basis—the value at the time of the original owner’s death. The inherited cost basis is typically “stepped up,” meaning you don’t pay taxes on value appreciation that occurred prior to inheritance. Instead, gains tax applies only to appreciation after you inherit the asset.

For example, if you inherit a house valued at $300,000 and sell it a year later for $350,000, the capital gains tax will apply to the $50,000 difference. Calculating the correct cost basis avoids overpaying on taxes and ensures compliance. When in doubt, seek advice from a tax pro or financial advisor familiar with the tax implications of your specific types of inherited assets, especially when dealing with mutual funds, stocks, or complex real estate holdings.

Cost Basis and Reporting Requirements After Inheriting Assets

Accurately establishing the cost basis of your inherited assets is critical for managing potential capital gains taxes. The cost basis generally resets to the asset’s market value at the time of the original owner’s death—but you must document this evidence, often with a professional appraisal for real estate or brokerage statements for mutual funds and stocks. If you receive an inherited IRA, cost basis and required distributions are governed by IRS rules specific to this account type.

Among your most important reporting duties are meeting IRS deadlines, filing forms like Form 706 (for estate tax reporting), and accurately disclosing cost basis when you sell inherited assets. Mishandling these requirements can lead to significant tax penalties. That’s why working with a financial advisor or tax pro ensures your paperwork is complete and your compliance is assured.

Step 4: Decide Whether to Invest, Save, or Pay Down Debt

Once your immediate needs and tax obligations are handled, it’s time to make strategic choices about what to do with the remainder of your inheritance. Should you invest in mutual funds, purchase real estate, contribute to retirement accounts, or keep more savings on hand? What you choose depends on your financial goals, risk tolerance, and overall plan. Start by assessing where your greatest opportunities for growth or stability exist.

For example, if you lack an adequate retirement nest egg, it may make sense to use your inheritance to max out your retirement account contributions. If your mortgage interest rate is much higher than average investment returns, paying down that debt could be a wise choice. Don’t rush—use a decision framework that reviews the potential returns and risks of each option. In many cases, a meeting with a financial advisor is well worth the investment, as they can help you balance saving, investing, and debt repayment in a way that works for your unique situation.

Should You Invest Your Inheritance? Exploring Mutual Funds, Real Estate, and Retirement Accounts

- Pros of Investing Inherited Assets: Potential for long-term growth, compounding returns, and diversification.

- Cons: Risk of market loss, fluctuating values, and timing concerns if you need quick access to funds.

Mutual funds offer diversified exposure to stocks, bonds, or other asset classes—minimizing the risk tied to a single investment. If real estate appeals to you, inherited funds can be used as a down payment or to purchase an investment property for rental income. For those focused on retirement, funneling inherited money into tax-advantaged retirement accounts—such as an IRA or 401(k)—can offer significant long-term benefits, subject to contribution limits. Consult your financial advisor before shifting large sums into investments to ensure they align with your financial plan and tolerance for risk.

Using Inheritance to Max Out Your Retirement Account or Inherited IRA

If your retirement savings have lagged or you recently received an inherited IRA, using your inheritance to fund these accounts offers compounding, tax-advantaged growth. With a traditional IRA or Roth IRA, you can grow your wealth tax-deferred or even tax-free (for a Roth). Check IRS annual contribution limits before depositing inherited money—if you’re rolling over from an inherited IRA, follow all required distribution rules to avoid penalties and gains taxes. Remember, rules for inherited IRAs differ from those for regular accounts, so working with a tax professional is essential to maximize your inheritance without triggering avoidable capital gains taxes.

Whether through retirement accounts or regular investing, the key is to match your choices to your timeline, goals, and risk tolerance. If you receive inherited assets with growth potential, such as stocks or mutual funds, consider letting them continue to grow rather than immediately cashing out.

Paying Off Debt versus Investing: A Decision Framework for Your Inheritance

Deciding whether to pay down debt or invest your inheritance is one of the biggest questions for new beneficiaries. Generally, if your debt carries a high interest rate—like credit cards—paying it off is financially superior to most investments. For lower-rate loans like home mortgages or student loans, compare the expected return if you invested your inheritance in the market versus the guaranteed return from debt repayment.

A simple framework: Pay off debts with rates above 6–8% first, while considering partial lump payments for lower rates in order to free up monthly cash flow. Next, review your investment options (such as mutual funds or real estate) and see if contributing to retirement accounts can boost your future earnings with minimal risk. Consulting a financial advisor will help clarify your options and design a strategy tailored to your needs and financial plan.

Step 5: Developing a Comprehensive Financial Plan After an Inheritance

Transforming your inheritance into long-term security requires a comprehensive financial plan. This plan should address both your immediate goals—like building an emergency fund—and your aspirations for the future, such as retirement, education funding, or charitable giving. Setting clear short-term and long-term goals keeps your decisions focused and prevents aimless spending. With your objectives mapped out, the next step is to create a diversified investment strategy that suits your age, risk profile, and timeline.

Re-evaluating your estate plan is also critical after you receive an inheritance. You may need to update beneficiaries, create or adjust trusts, and ensure your own family’s future is secure. Don’t forget: inheritance often changes your tax picture, so review your plans with a financial advisor and tax professional to ensure you’re making the most of new opportunities and minimizing liabilities.

Setting Short-Term and Long-Term Goals for Your Inherited Wealth

Short-term goals might include funding an emergency fund, paying off medical bills, or setting aside money for an upcoming major purchase. Long-term goals could involve building enough wealth to retire comfortably, paying for a child’s college, or creating a charitable trust. Make sure each goal is specific, measurable, achievable, relevant, and time-bound (SMART) for best results. By writing down your goals, you make your financial plan more concrete and hold yourself accountable for how your inherited funds are spent or invested.

Be realistic about what your inheritance can and cannot do—don’t put all your eggs in one basket or assume you can live off the sum indefinitely. Regular reviews with a financial advisor help you track progress and make adjustments as life changes.

Creating a Diversified Investment Strategy

Diversification is the cornerstone of growing your inheritance while reducing your risk. Build a portfolio that includes a healthy mix of asset classes: stocks for growth, bonds for stability, mutual funds for instant diversification, and possibly real estate for income and inflation protection. If you inherited substantial mutual funds, review their holdings to ensure they’re complementary to your entire investment mix, rather than overconcentrated in a single company or sector.

Real estate investments can also offer long-term price appreciation and rental income, but require active management and liquidity considerations. Speak to a financial advisor to develop a balanced strategy that reflects your goals, timeline, and comfort with risk. They can also help you optimize your investment choices for potential tax savings and capital gains minimization.

Adjusting Your Estate Plan and Beneficiaries Post-Inheritance

Inheriting money is often a wakeup call to review your own estate plan. Ensure wills and trusts are up to date and reflect your new financial situation. Adjust beneficiary designations across your retirement accounts, investment accounts, and insurance policies. Think about your long-term legacy and how you want your assets eventually distributed. Revisiting your estate plan now can also clarify strategies to minimize future estate tax or inheritance tax for your heirs.

This is a proactive step: don’t delay until the next life event. If you’re unsure how to update legal documents or strategize for future taxes, work closely with a financial advisor or estate attorney who specializes in inherited assets.

Step 6: Consulting a Financial Advisor After Receiving an Inheritance

When in doubt about tax implications, investment options, or building a financial plan, consult a seasoned financial advisor. These professionals bring expertise in inheritance planning, tax minimization, estate law, and diversified investment strategies. For most people, the modest cost of professional advice is far outweighed by the benefits of informed, optimized financial decisions—especially in the crucial months after you receive an inheritance.

Choose an advisor who is a fiduciary (bound to put your interests first) and has experience navigating estate tax, inheritance tax, and capital gains tax issues. They can also guide you through the process of managing inherited IRAs, mutual funds, brokerage accounts, and real estate for maximum financial benefit and minimum risk.

When to Hire a Financial Advisor for Inheritance Planning

You should hire a financial advisor if your inheritance involves complex assets (like business interests, real estate, or significant investment accounts), if you’re unsure about the tax consequences, or if you want to build a detailed, long-term financial plan. Advisors are invaluable when you’re faced with unique decisions, such as rolling over an inherited IRA, deciding whether to sell or keep inherited investments, or planning for future income tax responsibilities.

Even if your inheritance is relatively small, a one-time consultation can answer questions about capital gains taxes, cost basis, and the best order of steps to take. Their advice can help you keep more of your inheritance and create a legacy for generations to come.

How a Financial Advisor Can Help with Estate Taxes, Retirement Accounts, and Capital Gains

A knowledgeable advisor can assist you with estate tax calculations, plan withdrawals from retirement accounts like inherited IRAs, and make strategic recommendations for investing or saving inherited funds. They’ll ensure you’re maximizing every available tax benefit, managing risk, and constructing a plan that fits your specific needs. Your advisor can also coordinate with your tax pro to avoid double taxation on the same asset (such as both estate tax and gains tax on a property sale), and identify the most cost-effective order for managing or liquidating inherited assets.

As laws regarding capital gains taxes, estate tax, and account rules frequently change, working with a professional keeps your plan current and compliant. Having this support gives you peace of mind and confidence that your inheritance is working as hard for you as possible.

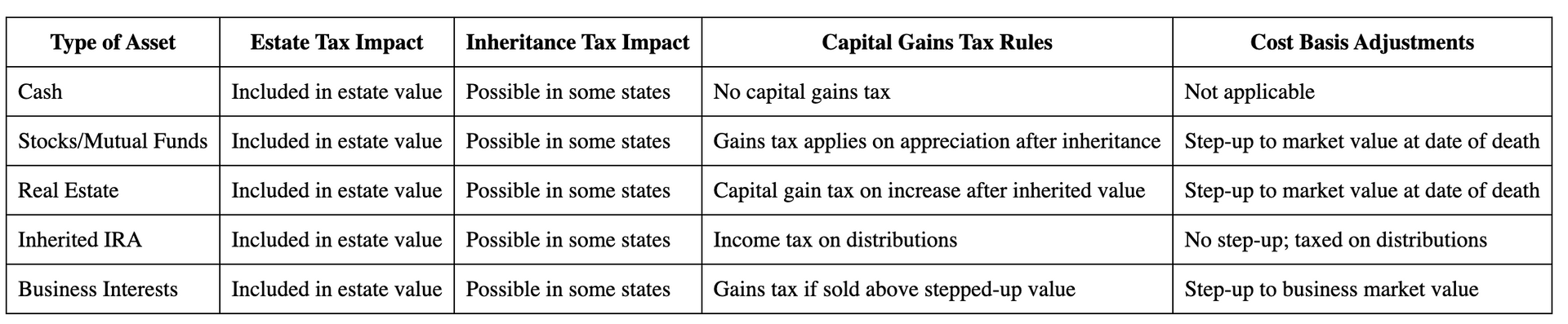

Table: Tax Considerations for Inherited Assets—Estate Tax, Inheritance Tax, and Capital Gains Tax

People Also Ask: What is the first thing you should do when you inherit money?

The Most Prudent Initial Step

The first thing you should do when you inherit money is pause and assess. Don’t rush into spending, investing, or giving it away. Take time to organize all inheritance-related documents, review potential tax obligations, and consider your options. Consulting a financial advisor during this period can help you understand complex assets (like real estate, mutual funds, or inherited IRAs) and set priorities. This allows you to make informed, well-planned decisions that sustain your inheritance for years to come.

People Also Ask: What to do if you inherit $100,000?

Optimal Ways to Use a Mid-Sized Inheritance

If you inherit $100,000, start by paying off high-interest debts, such as credit cards or personal loans, to immediately boost your financial health. Next, ensure you have a robust emergency fund. Consider contributing to your retirement accounts, such as a traditional IRA or Roth IRA, to secure your financial future. Then, based on your goals, you might invest a portion in mutual funds or real estate. Throughout the process, create a detailed financial plan and speak with a financial advisor to optimize tax efficiency and maximize the long-term impact of your inheritance.

People Also Ask: Is $500,000 a big inheritance?

Understanding the Impact of Significant Inheritances

Receiving $500,000 is a substantial inheritance for most households and can fundamentally change your financial outlook. It offers the ability to fully fund retirement accounts, invest in real estate or a diversified portfolio, pay down mortgage or other significant debts, and even plan for major future expenses like education or healthcare. However, a large inheritance also comes with higher stakes for tax obligations, investment risk, and long-term planning. The amount can seem endless, but disciplined planning is essential to ensure it provides lasting benefits rather than fleeting spending.

People Also Ask: What not to do with inheritance?

Common Mistakes to Avoid After Receiving an Inheritance

Some of the biggest mistakes to avoid after receiving an inheritance include: impulsively spending on luxuries, ignoring tax implications, failing to pay taxes where required, neglecting to update your financial plan or estate plan, and investing in unfamiliar or high-risk assets. Avoid giving away large sums to friends or relatives without considering your own long-term needs. Never overlook the importance of consulting a tax professional or financial advisor—expert guidance can prevent irreversible financial setbacks and help you get the most value from your inheritance.

A short educational video highlights the most common inheritance pitfalls—including impulse spending, missing tax deadlines, and poor planning—using simple, calming visuals and an authoritative voice for easy understanding.

"Proper planning can mean the difference between lasting security and financial regret after receiving an inheritance." — Magnum Financial Advisor

FAQs About What to Do with an Inheritance

- Is paying off my house with an inheritance always the best decision?

Not always. It depends on your mortgage’s interest rate, your financial goals, and current investment returns. If your rate is low, investing might bring higher returns. Assess your options with a financial advisor. - Will my inheritance be taxed twice?

Generally, no. Estate tax is charged at the estate level before distribution. However, capital gains or income tax may apply if you sell inherited assets or withdraw from retirement accounts. Consult a tax pro for your situation. - How should I manage inherited real estate or mutual funds?

Start by accurately determining the step-up cost basis. Decide whether to keep, sell, or reinvest based on your goals, tax implications, and market conditions. Professional appraisals and financial advice are invaluable here. - Can I use inherited funds to fund my child’s education or retirement accounts?

Absolutely. You can contribute to 529 plans, custodial accounts, or your own IRA (subject to annual limits). Always factor in taxes, your personal needs, and long-term plans before reallocating inherited funds.

Key Takeaways: What to Do with an Inheritance Effectively

- Pause and assess before taking action

- Prioritize emergency fund and debt repayment

- Understand and address estate tax, inheritance tax, and capital gains

- Make informed decisions on investing or saving

- Seek professional financial advice when needed

Secure Your Future—Call Magnum Financial today at 707-996-9664 or email us at sbossio@magnum-financial.com

Your inheritance is more than a windfall—it’s a unique chance to secure your family’s future. Take deliberate steps, avoid common mistakes, and build a legacy that endures. Start your journey with Magnum Financial’s expert guidance today!

Sources