Inheritance Budgeting Tips That Could Save You Money Today

Did you know that nearly 70% of inherited wealth is lost by the second generation? Managing an inheritance isn't just about splurging—it's about making smart, timely decisions that safeguard your windfall for decades to come. Whether you've just received an inheritance or expect one soon, learning strategic inheritance budgeting tips could be the difference between a secure future and a costly mistake.

Unlocking the Power of Inheritance Budgeting Tips – Startling Statistics and Little-Known Facts

Statistics reveal that most heirs are unprepared for the complexities of inherited wealth, leading to preventable losses and missed opportunities. In fact, studies show over 60% of recipients struggle with planning and budgeting following a significant inheritance. These lost fortunes often stem from emotional spending, overlooking tax implications, and failing to integrate inherited assets into an organized financial plan or estate plan. Today, you can join a savvy minority who take a strategic approach to managing windfalls—setting up multi-generational security and giving their families a lasting legacy.

Let’s uncover the little-known facts about inheritance budgeting tips—including how to optimize large inheritances, use advanced tax strategies, and make the right financial decisions right after you receive an inheritance. Throughout this article, you’ll get actionable steps, expert advice, and real-world examples that can help you turn inherited wealth into a foundation for future success.

What You'll Learn: Mastering Inheritance Budgeting Tips for Financial Success

- How to optimize inherited wealth for both short- and long-term stability

- Key inheritance budgeting tips that help avoid common pitfalls

- Practical strategies for effective estate planning, estate tax management, and legacy building

- Expert recommendations for aligning inherited funds with your financial goals

The Importance of Inheritance Budgeting Tips: Why Every Heir Needs a Plan

Inheriting money is often an emotional time, making it easy to overlook key steps in financial planning. Without a clear plan, many quickly deplete their windfall or find themselves tangled in tax issues and unforeseen liabilities. Inheritance budgeting tips empower recipients to make intentional choices, protecting both the value of the inheritance and their future financial wellbeing. Establishing an estate plan, understanding estate tax and inheritance tax obligations, and setting achievable financial goals guarantee your inherited wealth benefits you and generations to come.

Immediate access to substantial funds is both a privilege and a responsibility. Gaining clarity about your financial situation—from existing debts to new investment opportunities—lets you align inherited resources with personal and family objectives. By following expert inheritance budgeting strategies now, you set the stage for a more secure financial life. "Proper budgeting can preserve an inheritance for generations to come. " — Financial Planner

Step 1: Assess Your Financial Situation When You Receive an Inheritance

Receiving an inheritance can shift your entire financial landscape in an instant. That’s why your first step should be to halt any immediate spending, no matter how tempting. Begin by reviewing your current financial situation: list debts, existing assets (like a savings account or real estate), and ongoing obligations. Next, gather documentation related to your inherited assets—bank statements, will or estate plan documents, and investment records. Understanding your new position is the foundation of any solid financial plan.

This is also a good time to reflect on your personal and family financial goals. Do you want to pay off debt, buy a home, fund an emergency fund, or invest for retirement? Quantifying your goals will inform how best to deploy your inheritance. Remember, the type of assets you inherit—cash, stocks, or real estate—will also affect your decisions. Consulting a legal or financial advisor is highly recommended to ensure you comply with local laws and get help integrating inherited wealth into your broader planning.

Understanding Inherited Wealth and Personal Financial Goals

- Immediate steps after receiving an inheritance

- Evaluating your financial goals and current obligations

- Taking stock of inherited assets and liabilities

Step 2: Identify and Manage Tax Implications with Inheritance Budgeting Tips

One of the most critical inheritance budgeting tips is understanding the tax implications of inherited wealth. Both estate tax and inheritance tax can take a substantial bite out of your windfall if left unmanaged. The 7 year rule on inheritance—a principle affecting gifts made before death—affects how much tax is due based on timing, which can catch heirs off guard. Reviewing inherited retirement accounts also requires careful planning because distributions may trigger immediate taxation or special rules, especially for large balances.

Tax laws vary greatly based on jurisdiction, asset type, and whether you’re inheriting retirement accounts, life insurance, or other investments. Consult with a tax advisor or financial planner to determine tax rules specific to your situation and to incorporate professional estate planning techniques into your overall strategy. Effective tax management means recognizing opportunities to defer, minimize, or spread out liabilities, thus preserving more of your inheritance for future financial needs.

Estate Tax, Inheritance Tax, and Retirement Accounts

- How estate tax and inheritance tax affect your assets

- The 7 year rule on inheritance explained

- Managing retirement accounts for maximum benefit

- Navigating tax implications with proper estate planning

Step 3: Create a Comprehensive Estate Plan and Financial Plan

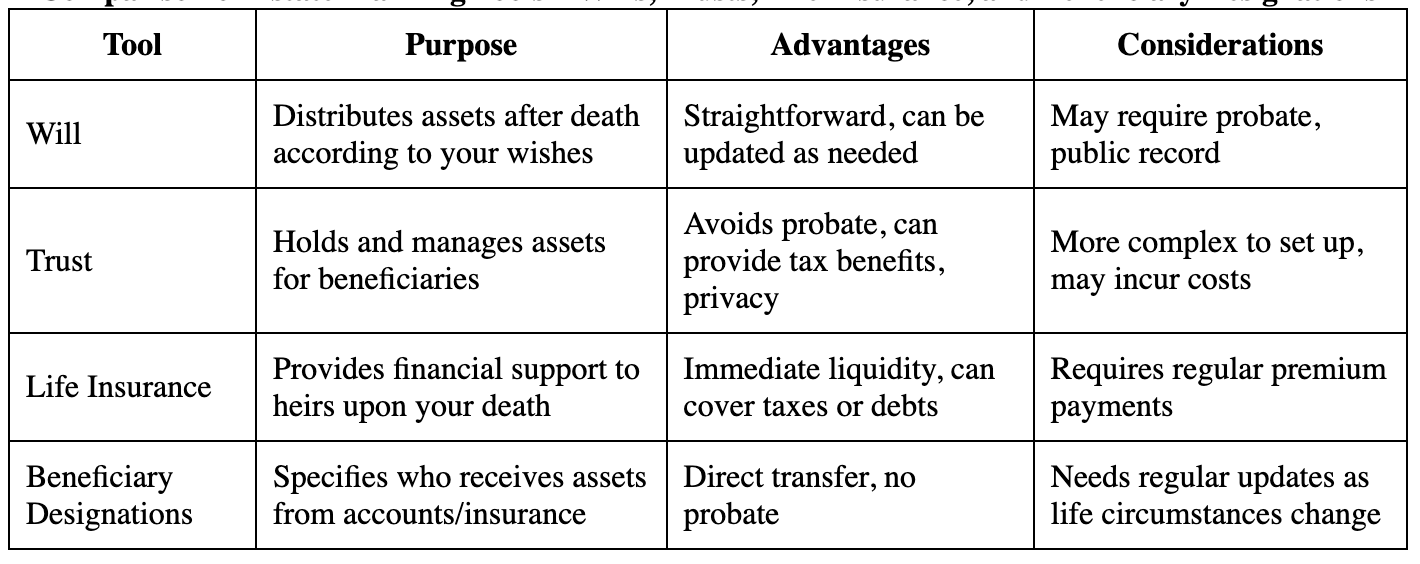

Every major life change—including a new inheritance—should prompt a review or creation of a comprehensive estate plan and financial plan. A solid estate plan consists of more than just a will; it can also feature trusts, powers of attorney, healthcare directives, and thoughtful beneficiary designations. Life insurance policies, meanwhile, offer liquidity to heirs and can help manage estate tax or inheritance tax liabilities.

Align your estate plan with estate planning best practices to prevent assets from entering probate, reduce tax exposure, and protect your legacy. Work with a professional who can tailor recommendations to your specific situation and future financial ambitions. By proactively organizing your affairs, you remove much of the stress that can accompany transitions and ensure your wishes are executed smoothly.

Estate Planning, Life Insurance, and Future-Proofing Your Inheritance

- Components of an effective estate plan

- The role of life insurance and trusts

- Aligning your estate plan with estate planning best practices

Comparison of Estate Planning Tools – Wills, Trusts, Life Insurance, and Beneficiary Designations

Step 4: Budget Your Inheritance: Key Inheritance Budgeting Tips for Smart Spending

Once you have an estate plan in progress, it’s time to set up a practical budget tailored to your new financial circumstances. A popular inheritance budgeting tip is the 70-10-10-10 budget rule, which helps you allocate funds thoughtfully and resist impulsive spending. This rule guides you to divide your inheritance as follows: 70% for necessities and lifestyle, 10% for savings, 10% for investment growth, and 10% for charitable giving or philanthropy.

Implementing a structured budget ensures you cover essentials while also planning for your future and investing in causes that matter. If you receive a large inheritance, a budget keeps emotions in check and leaves little room for financial regrets. Always be sure to reconcile your financial decisions with both immediate needs and future goals, like building your retirement plan, enhancing your emergency fund, or contributing to a savings account.

Implementing the 70-10-10-10 Budget Rule for a Large Inheritance

- What is the 70-10-10-10 budgeting method?

- Applying the method to inherited wealth

- Setting financial goals that align with windfall gains

Real-World Advice from Estate Planning Professionals

Seasoned estate planning experts emphasize the importance of pausing before making significant financial moves. Their #1 advice? Engage a financial advisor early and remain aware of your emotional state. They caution heirs to beware of common inheritance pitfalls like underestimating estate tax or not factoring in the unique rules around inherited retirement accounts. Their insight: “Treat your inheritance as part of your overall financial plan, not as a windfall to be spent swiftly. Strategic planning can turn an inheritance into a long-term financial safety net for your family. ”

Step 5: Invest Inherited Wealth Wisely Using Proven Inheritance Budgeting Tips

The next step is to invest inherited wealth in a way that balances growth, security, and your unique financial goals. Diversifying your portfolio is essential—avoid placing all inherited assets in one account or investment type. Use a mix of stocks, bonds, real estate, and, where appropriate, retirement plan vehicles. Respect your personal risk tolerance: if you’re nearing retirement, you may want more stable options. If you’re younger, a long-term perspective could justify more aggressive growth investments.

Smart inheritance budgeting tips for investing include making strategic retirement account rollovers, which can offer long-term tax benefits. An experienced financial advisor can help you select vehicles that match your timeframe and future financial needs. Remember, investing isn’t about chasing trends—it’s about crafting a strategy that grows wealth over time while shielding it from excessive risk and taxes.

Aligning Investments with Long-Term Financial Goals

- Diversifying your inherited portfolio

- The importance of risk tolerance and timeframe

- Using retirement account rollovers strategically

Step 6: Adjust Your Financial Goals for a New Financial Situation

Inheriting assets may require a complete reset of your short-term and long-term financial goals. Take time to consult with your financial advisor to reevaluate what success looks like in this new chapter. You may choose to enhance your emergency fund, initiate philanthropic contributions, or accelerate retirement planning. This is the perfect moment to update or create a robust financial plan that aligns with your expanded resources and objectives.

Don’t forget to account for ongoing and potential estate tax or inheritance tax liabilities as you plan for future wealth distributions to your heirs. Strategic adjustments to your estate plan can protect your assets and set your loved ones up for future success. As circumstances and laws are subject to change, commit to regular plan reviews to ensure your decisions remain optimal.

Establishing Short-Term and Long-Term Plans for Inherited Funds

- Adjusting your financial plan after a large inheritance

- Planning for future estate tax and inheritance tax liabilities

Lessons Learned from Heirs Who Maximized Their Inherited Wealth

Heirs who sought professional guidance—especially from financial advisors and estate planners—consistently reported better long-term outcomes. From setting up trusts and budgeting for tax liabilities to building diverse investment portfolios, these real-world examples underscore the tangible benefits of careful, deliberate inheritance budgeting. One common theme: those who avoided impulsive decisions and stuck to a written financial plan preserved and grew their inherited assets, while those who acted hastily often faced steep tax bills or diminished wealth. Their top advice: “Take your time, do your homework, and let your goals—not your emotions—drive your decisions. ”

Key Inheritance Budgeting Tips to Protect and Grow Your Wealth

- Consulting professionals early

- Keeping thorough records of all estate plan documents

- Understanding tax implications before making decisions

- Regularly reviewing your financial and estate plans

People Also Ask: What is the first thing you should do when you inherit money?

Answer: Reviewing immediate financial needs and seeking advice from a financial planner are essential first steps for anyone who receives an inheritance.

People Also Ask: What is the 7 year rule on inheritance?

Answer: The 7 year rule on inheritance, often relating to gifts, impacts how much inheritance tax is due depending on the time elapsed since the gift was made.

People Also Ask: What is the 70-10-10-10 budget rule?

Answer: The 70-10-10-10 rule suggests allocating 70% of funds for essentials, and 10% each to savings, investing, and philanthropy, making it ideal for managing a large inheritance.

People Also Ask: What is the most common inheritance mistake?

Answer: The most common inheritance mistake is spending impulsively without considering tax implications, estate planning, or long-term financial goals.

Frequently Asked Questions about Inheritance Budgeting Tips

What documents should you gather after inheriting wealth?

After inheriting, collect all relevant documents: the will, trust (if any), insurance policies, deeds and titles for real estate, retirement account statements, bank letters, tax forms, and any records concerning estate taxes or inheritance tax payments. Having these documents organized will streamline the process of executing the estate plan and consulting with professionals.

How can you minimize estate tax and inheritance tax?

Work with a financial advisor or tax professional who understands current tax rules and estate planning strategies. Techniques include gifting strategies, establishing trusts, maximizing lifetime gift exemptions, and structuring investments to reduce taxable exposure. Each situation is unique, so personal guidance is crucial to minimize liabilities.

Is it possible to roll over inherited retirement accounts?

Yes, but the options and rules differ depending on the account type (IRA, 401k, etc. ), your relationship to the deceased, and specific IRS guidelines. Generally, non-spousal heirs must follow strict distribution requirements, but spousal heirs often have more flexibility. Consult a retirement account specialist to ensure compliance and maximize tax advantages.

When is the best time to update your estate plan after receiving an inheritance?

You should review and update your estate plan as soon as possible after receiving an inheritance. Integrating new assets, adjusting beneficiaries, and revising plans for estate tax and inheritance tax exposure will ensure your wishes are clearly documented and protect your family’s financial future.

Key Takeaways: Maximizing the Value of Inheritance Budgeting Tips

- Planning and budgeting are crucial to growing and protecting inherited assets

- Consulting pros can help navigate estate tax and inheritance tax complexities

- Leveraging professional guidance delivers long-term financial confidence

Ready to Take Control? Call Magnum Financial today at 707-996-9664 or email us at sbossio@magnum-financial.com

Conclusion: Maximize the value of your inheritance by planning, budgeting, and seeking expert advice today—you’ll thank yourself and so will your family for generations to come.

Sources

- Investopedia – Inheritance: What to Do With Inherited Money

- Kiplinger – Estate Planning

- IRS – Estate Tax

- Forbes – Inherited IRA Rules

- Fidelity – Managing an Inheritance