Struggling with Managing Inherited Assets? Here’s Help

Did you know? Nearly 70% of wealth transfers are lost by the second generation, and an astonishing 90% by the third, often due to poor management of inherited assets. This means most people who inherit assets face far more pitfalls than they realize. If you’ve recently come into an inheritance—whether it’s property, life insurance, investments, or family heirlooms—navigating the legal, financial, and emotional terrain can be overwhelming. In this comprehensive guide, you’ll discover how managing inherited assets doesn’t have to be a struggle. With clear steps and expert strategies, you can safeguard your inheritance and turn it into a foundation for long-term financial growth.

A Surprising Reality: Why Managing Inherited Assets Proves Challenging

- In the U.S., only about 30% of inherited wealth lasts through the second generation, with mismanagement and family disputes often to blame.

What You'll Learn About Managing Inherited Assets

- How inheritance tax, capital gain, and cost basis affect your bottom line

- The essentials of an estate plan and the value of a financial advisor

- Best practices for managing inherited real estate, retirement accounts, and life insurance proceeds

- Steps to define your financial goals and build a solid financial plan

- Strategies for handling family dynamics and preserving your legacy

Understanding the Basics of Managing Inherited Assets

At its core, managing inherited assets means taking legal and financial responsibility for wealth or property left behind by a loved one. This includes more than just money—it could be real estate, investment portfolios, life insurance policies, retirement accounts, valuables, and business interests. A well-executed estate plan is essential to make sense of these assets and ensure a smooth transfer. Without proper guidance, the process easily becomes overwhelming due to legal complexities and emotional strain. Understanding the fundamentals prepares you to make informed decisions and reduce stress during what can be a challenging time.

The cornerstone of effective management is knowing what’s in the estate plan, if one exists. Estate planning documents detail who inherits what, how assets should be distributed, and whether there are trusts, wills, or beneficiary designations in place. Partnering with professionals—such as an estate attorney, tax professional, or financial advisor—can expedite the process and protect you from costly mistakes. Their expertise helps you interpret legal terms, understand state tax implications, and navigate probate court as required by state law.

As you navigate the complexities of inherited assets, it's also important to understand how these decisions fit into your broader financial picture. For a deeper dive into building a comprehensive financial plan that incorporates new wealth, consider exploring how to create a financial plan after receiving an inheritance—a resource that offers actionable steps for integrating your windfall into long-term goals.

Defining Inherited Assets: What Falls Under Your Control

- Inherited assets span a wide spectrum: cash, real estate properties, stocks, bonds, retirement accounts (like an IRA or 401(k)), life insurance policies, collectibles, and even family businesses.

- A comprehensive estate plan typically includes a will, trust documents, powers of attorney, and beneficiary designations—all determining what you inherit and your rights as an heir.

Inherited assets are not always straightforward. For instance, you might inherit a vacation home along with maintenance expenses, or receive a life insurance payout with unique tax rules. Understanding which items fall under your control—and which are tied to shared ownership with siblings or co-heirs—shapes how you manage them going forward. Review all documentation thoroughly; this could include property deeds, financial account statements, and the deceased’s will or trust documents.

Typical Challenges in Managing Inherited Assets

- Inheritance taxes and legal hurdles: Not all states impose inheritance taxes, but those that do can significantly reduce the value you receive. Calling on an experienced tax professional helps identify your liability, especially if state tax or federal estate tax applies.

- Emotional decision-making: Grief often clouds judgment. Rushing the sale of cherished assets or overlooking key steps—like appraising real estate—are common pitfalls.

- Valuation struggles: Determining the fair market value for collections, jewelry, or a business can be intricate. Getting professional appraisals is crucial for tax-reporting and equitable division among heirs.

"Proper management of inherited assets often determines whether wealth is preserved or lost within a generation." — Financial Advisor, Magnum Financial

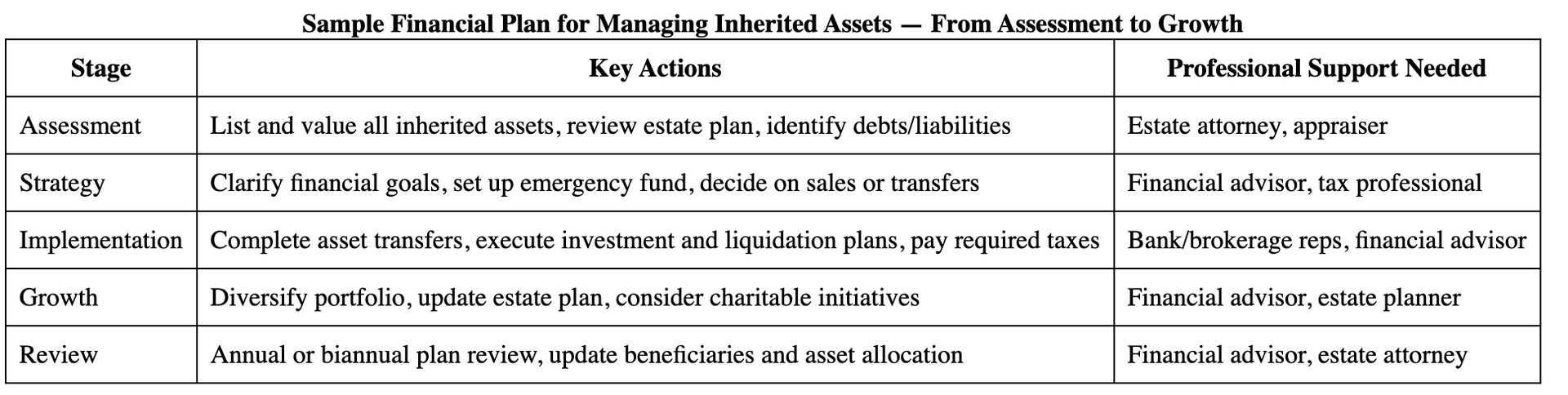

First Steps When Inheriting Assets: Building a Smart Foundation

- Notify relevant institutions and beneficiaries

- Organize and secure all necessary documentation

- Engage a financial advisor or estate attorney early in the process

After notification of your inheritance, the paperwork may seem endless. Begin by gathering and securing all estate documents, then notify financial institutions, insurance companies, or brokerage firms about the change in asset ownership. Simultaneously, seek professional guidance from a financial advisor and review your estate plan to understand your liabilities, obligations, and next steps before making any withdrawals or sales. Having a credible team of professionals protects your interests and ensures critical legal requirements are not missed.

Before making any decisions, pause to outline your financial situation and set clear financial goals. For many, receiving an inheritance brings new hope but also unexpected pressures. Establish an emergency fund, assess your debts, and consider how the inheritance fits both short- and long-term financial needs. Aim to design a holistic financial plan—one that protects your new wealth and moves you closer to independence.

Identifying Inherited Assets and Assessing Value

- List all inherited property: real estate, life insurance payouts, investment accounts, retirement plans, and physical assets like cars or art.

- Get formal appraisals or statements of value for real estate, jewelry, collections, business interests, and vehicles.

Start by identifying everything you’ve inherited—sometimes, this means combing through family documents or waiting for probate court to rule. Assign a fair market value to each asset, capturing the full picture for tax filing. Many financial advisors recommend using a simple spreadsheet to keep track, noting account numbers, contact information for custodians, and relevant legal documentation. For real estate, secure an independent appraisal to satisfy both taxation and equitable distribution requirements.

Assessing Your Financial Situation and Setting Financial Goals

- Review your cash flow, debts, and how inherited assets can improve your financial situation

- Consult with a financial advisor to chart your financial plan—considering emergency fund needs, investment strategies, retirement planning, and new financial goals

Don’t view your inheritance as a windfall to spend impulsively. Instead, integrate it into a realistic financial plan. Decide whether to pay off debts, invest for future growth, or earmark funds for education or a home purchase. A detailed review with an advisor can reveal opportunities for tax savings, risk diversification, and enhanced wealth management. Define your financial goals upfront so your inheritance becomes a springboard for lifelong prosperity instead of a fleeting windfall.

Video Guide: The First Things to Do When Managing Inherited AssetsManaging Inherited Assets: Navigating Taxes and Legal Requirements

Taxes and legal obligations are some of the most daunting aspects of managing inherited assets. While federal estate tax only applies to larger estates, state law may impose inheritance or estate taxes at lower thresholds. Income tax and capital gains tax rules might differ for each asset type, especially for investments and real estate. Understanding the differences and creating a sound financial plan can help you avoid costly surprises. Consulting a tax professional with expertise in inheritance taxes will ensure compliance and strategic tax reduction.

Beyond taxes, legal processes—such as probate or reviewing trust documents—demand careful attention. Each state has unique laws, and the structure of the estate plan can determine how long and complex the process becomes. Always seek legal advice to understand your obligations and options before distributing or liquidating assets.

Inheritance Tax and Inheritance Taxes: What You Need to Know

- Inheritance tax varies by state, while estate tax is imposed at the federal level for certain high-value estates.

- Capital gains tax may apply when inherited investments or property are sold, depending on the original cost basis and sale value.

It’s vital to differentiate between these taxes: inheritance tax is levied on heirs based on their share, estate tax is deducted from the estate before distribution, and capital gains tax is due only upon the sale of inherited assets that have appreciated in value. Not every state enforces inheritance taxes, but those that do can reduce your final inheritance by several percentage points.

Cost Basis, Capital Gain, and Capital Gains on Inherited Investments

- A step-up in cost basis resets the asset’s value to fair market value at the date of death, reducing potential capital gains tax when you sell.

Inherited investments and real estate typically receive a “step-up in cost basis.” For example, if your parent bought stock for $10,000 and it’s worth $50,000 at inheritance, your new cost basis is $50,000—not $10,000. If you sell soon after, you may incur little or no capital gain, keeping your tax bill low. This benefit can be substantial, especially for highly appreciated assets. Work with a tax professional to accurately record the new cost basis and ensure you’re leveraging this break under current tax rules.

For assets that appreciate after being inherited, any gains above the new cost basis are subject to capital gains tax. Keeping records of appraisals and valuations at the time of inheritance is critical. Your financial advisor can help track these values and suggest the best timing for sales to minimize tax impact.

Strategies to Minimize Capital Gains Taxes on Inherited Money

- Sell assets soon after inheriting, when the new cost basis is highest.

- Consider gifting appreciated assets to charities for tax deductions.

- Work closely with a financial advisor or certified tax professional to utilize legal strategies within the tax rules of your state and the IRS.

Minimizing taxes starts with smart timing and documentation. If you sell investments or property quickly, post-inheritance gains are likely to be minimal—and so is your capital gains tax. For those who prefer to keep inherited assets, periodic portfolio reviews and conversion strategies (such as moving appreciated stock into a donor-advised fund) can help reduce liabilities. Always confirm your approach with professionals versed in both federal and state tax law.

Life Insurance, Retirement Accounts, and Real Estate: Managing Specialized Inherited Assets

Certain assets require specialized management. Whether you’re handling a life insurance payout, an inherited IRA (retirement plan), or real estate, each carries unique legal and tax implications. For instance, the way you claim or transfer a beneficiary IRA differs dramatically from a bank account. Real estate comes with maintenance, taxes, and market considerations—while life insurance payouts may be tax-free but could bump you into a higher income tax bracket. Knowing these distinctions is the key to safeguarding your inheritance.

How to Handle Life Insurance Payouts When Managing Inherited Assets

- Most life insurance payouts are income tax–free, whether you take them as a lump sum or an annuity.

- If a policy has an investment component, or is cashed out before death, taxes may apply—consult your financial advisor or tax professional for your specific situation.

As a beneficiary, you usually receive life insurance proceeds tax-free. However, choosing a lump-sum payment gives you immediate control, while annuity payouts spread the distribution (and interest earnings) over multiple years, which may have tax consequences. If the policy owner died with the payout as part of their taxable estate, estate taxes may apply depending on the estate’s size and the state’s laws. Always evaluate your options—sometimes rolling proceeds into a retirement or savings account aligns better with your broader financial goals.

Managing Inherited Retirement Accounts: Key Decisions

- Inherited IRAs and other retirement accounts may require required minimum distributions (RMDs) based on your age and status as spouse/non-spouse beneficiary.

- Early withdrawals could lead to penalties or additional income tax—knowing current rules and deadlines is critical.

IRS rules on inherited retirement accounts are complex and frequently change. Spouses typically have more options, such as rolling the account into their own IRA, whereas non-spouses often must withdraw the full balance within 10 years. Failure to follow RMD schedules can trigger substantial penalties. Review accounts—such as a traditional IRA or 401(k)—with a financial advisor familiar with estate planning and the latest tax rules. Their insights preserve more of your inheritance while avoiding unnecessary penalties and income taxes.

Real Estate Considerations in Managing Inherited Assets

- Obtain a professional appraisal to establish current market value and cost basis for tax purposes.

- Weigh the benefits of keeping versus selling: factor in property taxes, upkeep, potential rental income, and your family’s financial goals.

Inherited real estate brings both opportunity and responsibility. Market conditions, property location, and personal/family preferences should all shape your decision. Selling may provide immediate funds and reduce headaches around maintenance and taxes, while keeping property as a rental can generate ongoing income. Remember: when you sell, any gain over the stepped-up cost basis is subject to capital gain tax. Discuss options with a real estate agent and financial advisor to maximize value and avoid tax surprises.

Working with a Financial Advisor to Optimize Your Inherited Assets

- Accessing professional advice ensures you don’t overlook tax, legal, or investment pitfalls common to inherited assets.

- A financial advisor helps create a tailored financial plan, revises your estate plan, and optimizes asset allocation—ensuring long-term growth.

Few people are prepared to manage a significant, unexpected windfall. A skilled financial advisor brings invaluable expertise: from setting up a holistic financial plan to implementing tax-advantaged strategies across different types of inherited assets. They’ll help you set financial goals, rebalance your investment portfolio, and periodically review your estate plan. This ensures your new wealth is protected for future generations—and that you avoid mistakes that threaten your inheritance’s value.

Pro tip: Regular meetings with your advisor can keep your plan current with tax law changes, fluctuating markets, and evolving family circumstances. Personalized guidance is especially important in blended families or when handling inheritance with siblings. They can also facilitate difficult family conversations and avoid costly probate court battles.

Selecting the Right Financial Advisor for Managing Inherited Assets

- Seek a credentialed advisor with expertise in estate planning, tax law, and wealth management for heirs.

- Look for transparent fees, fiduciary responsibility, and proven experience dealing with similar inheritance cases.

Not all advisors are created equal. Interview several candidates, asking about their experience with estate plan reviews, navigating inheritance tax issues, and integrating newly acquired assets into a broader financial plan. Trust is critical—choose someone who listens, explains options clearly, and tailors recommendations for your unique financial situation. Confirm whether they are a fiduciary, meaning they are legally bound to act in your best interest. Additionally, ensure they understand your state laws and can collaborate with your estate attorney.

Managing Family Dynamics: Inheritance with Siblings and Heirs

Inheritance can strain even close-knit families. Disputes often arise over sentimental items, fairness in distribution, and decisions regarding shared assets like real estate. An up-to-date, clearly worded estate plan is essential to minimize conflicts, but communication and compromise remain key. Preserve both assets and relationships by approaching these discussions calmly and transparently.

Best Practices for Managing Inheritance Property with Siblings

- Hold regular, honest discussions with all heirs to ensure clear understanding and transparency.

- If necessary, use a neutral mediator or estate attorney to resolve disputes and ensure the estate plan is followed to the letter.

- Consider buyouts or the sale-and-split approach for shared real estate; written agreements among siblings help avoid future misunderstandings.

Many families successfully co-own inherited assets by outlining each person’s responsibilities and rights in writing. If consensus is hard to reach, it may be best to liquidate shared assets and split proceeds. Remember, the most important legacy is often the family relationship itself—never underestimate the value of compromise and professional guidance in difficult times.

"Transparent discussion and written agreements between siblings can preserve relationships and assets alike." — Estate Planning Expert

Creating a Long-Term Financial Plan After Managing Inherited Assets

With the immediate decisions behind you, focus shifts to maximizing and preserving your inherited wealth for decades to come. This requires a diligent, forward-thinking financial plan—balancing current needs, future growth, and your broader financial goals. Updating your estate plan regularly is equally critical, ensuring your own heirs are positioned to inherit efficiently and peacefully.

Investment Strategies and Protecting Your Wealth

- Align new assets with your personal financial goals: retirement planning, education funding, travel, or philanthropy.

- Diversify investments across stocks, bonds, real estate, and alternative assets to mitigate risk.

- Update your estate plan to reflect changes and establish clear beneficiary designations.

Preserving your new wealth requires sophisticated investment strategies. Consider collaborating with an advisor to create a diversified, tax-efficient portfolio. Layer on risk management and periodically review your progress toward your financial goals—this ensures your inheritance supports your lifestyle both now and in retirement. Regular estate planning check-ins keep your own heirs from facing the same challenges you encountered.

Philanthropy and Charitable Giving: Leveraging Your Inherited Assets

- Explore donor-advised funds or direct gifts to charities, which can provide generous tax breaks and create a legacy of giving.

- Consult your advisor to structure gifts in ways that reduce estate tax and maximize long-term impact.

If you wish to honor a loved one’s memory or support your community, charitable giving can be woven into your estate and financial plan. Options range from simple annual donations to the creation of foundations or trusts. Beyond tax advantages, donating part of your inheritance can provide personal fulfillment and affirm the legacy you want to leave for future generations.

People Also Ask: Managing Inherited Assets FAQ

What is the first thing you should do when you inherit money?

- Secure the funds and assess liabilities—don’t spend or invest immediately.

- Notify financial institutions and gather all documentation.

- Consult a financial advisor or tax professional to tailor guidance for your specific situation and asset requirements.

Taking these first steps gives you the clarity and confidence needed to make smart, informed decisions for your long-term financial future.

What is the 7 year rule for inheritance?

- This rule typically applies in some countries where gifts given by the deceased are exempt from inheritance taxes if the giver survives for seven years after making the gift.

The 7 year rule reduces or eliminates tax liability on gifts as they “age” beyond seven years from the giver’s passing, a significant planning strategy in jurisdictions such as the UK.

What is the best way to manage inheritance property with siblings?

- Reach consensus early; written agreements prevent misunderstandings.

- Consider options like co-ownership, buyouts, or selling and dividing proceeds after fair market appraisal.

Open communication, legal contracts, and sometimes mediation help families preserve both relationships and asset value when managing inherited real estate together.

How to avoid capital gains on inherited money?

- Leverage the step-up in cost basis—assets are revalued at death, reducing taxable gains if sold soon after inheritance.

- Work with your financial advisor and tax professional for legal tactics enabled by tax law to minimize or defer taxes.

Quick sales, charitable gifting, and specific trust setups all offer ways to reduce or avoid capital gains tax on inherited investments and property.

Frequently Asked Questions on Managing Inherited Assets

- What should I do with inherited real estate—keep, sell, or rent?

- How are inherited retirement accounts like IRAs or 401(k)s handled?

- Do I owe state or federal inheritance taxes on a life insurance payout?

- Should I use my inheritance to pay debts or invest for the future?

- How do I update my estate plan after receiving an inheritance?

Key Takeaways for Effectively Managing Inherited Assets

- Document everything—assets, valuations, and liabilities

- Handle tax management proactively with professional support

- Rely on expert advice for legal and financial complexities

- Regularly review your financial goals and keep your estate plan current

Ready for Expert Guidance?

- Call Magnum Financial today at 707-996-9664 or email us at sbossio@magnum-financial.com to ensure your inherited assets are managed with expertise and care.

Conclusion: Secure Your Legacy by Managing Inherited Assets Wisely

- Thoughtful and proactive management of inherited assets, in partnership with trusted professionals and a well-structured estate plan, ensures your financial legacy is preserved and built for generations to come.

Managing inherited assets is just the beginning of your journey toward lasting financial security. If you’re ready to take your wealth stewardship to the next level, consider broadening your perspective with advanced estate planning and legacy strategies. Discover how proactive planning can help you protect your family’s future and optimize your financial impact by visiting estate planning strategies for multigenerational wealth. By deepening your understanding, you’ll be empowered to make decisions that not only honor your inheritance but also build a legacy for generations to come.